designer491

Understanding the 2022 Investment Landscape

The year 2022 has been challenging for investors, marked by significant downturns across various markets. The S&P 500 has dipped into a bear market, tech stocks that previously thrived have taken a hit, and bond performances have also been disappointing. This ongoing trend could extend into 2023 as persistent macroeconomic challenges continue to affect market stability and investor confidence.

However, there’s a silver lining for those who prioritize conservative investing strategies. Investors focusing on low-volatility dividend growth stocks have managed to outperform the broader market this year, successfully capitalizing on more favorable valuations while mitigating risks associated with market fluctuations.

In this article, I aim to delve into the current macroeconomic landscape and highlight the importance of investing in quality dividend growth stocks. Additionally, as suggested in the title, I will present three of the highest-quality dividend stocks that investors can consider adding to their portfolios.

Given the recent drop in stock prices, many are curious about where to allocate their funds. This often involves discussions around portfolios ranging from $10,000 to $20,000, which is a common starting point for many retail investors.

By mentioning $10,000 in the title, I aim to resonate with retail investors who are beginning their investment journey. Investing this amount in a single stock can be an excellent way to kickstart a long-term investing strategy.

This article emphasizes quality investments. I will be discussing three stocks that I would recommend even to those with limited market knowledge—stocks that provide peace of mind, feature robust balance sheets, offer decent yields, and exhibit promising dividend growth.

In essence, these are three of the best stocks available for investment.

Let’s dive in!

Navigating Market Uncertainties in 2022

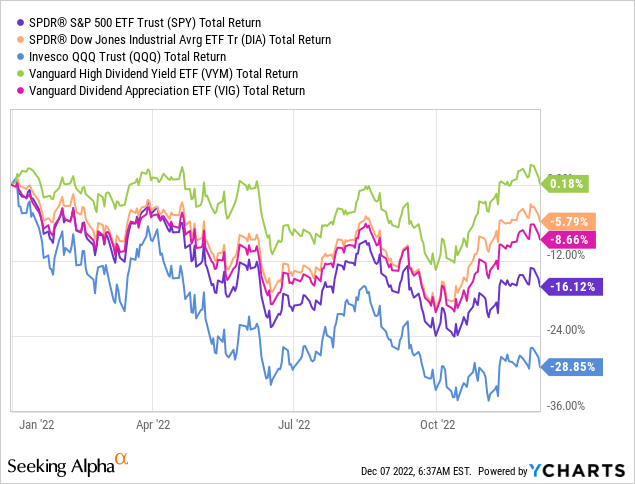

This year, the S&P 500 has experienced a decline of 16%, including dividends, which is a stark contrast to the 24% loss recorded in October and significantly higher than the 29% drop seen in the tech-heavy ETF (QQQ). Interestingly, the Dow Jones has fared better, with a decrease of less than 6%. In fact, many high-yield dividend stocks have managed to remain in positive territory!

This year has underscored the divergence between growth and value stocks. Factors such as a rising interest rate environment, slower economic growth, and a proactive Federal Reserve have led investors to shy away from growth stocks that previously performed well.

While many growth stocks that struggled in 2022 had previously thrived, this situation serves as a reminder of the core principles of investing: acquiring stocks that thrive in bull markets while simultaneously safeguarding against potential downturns in bear markets.

Identifying stocks with this dual capability is crucial for long-term investment success.

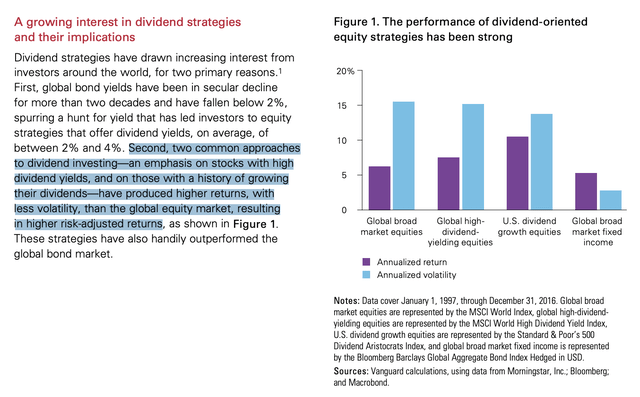

Vanguard has aptly illustrated that investing in quality dividend growth stocks can yield superior returns compared to the broader market while experiencing lower volatility. The accompanying chart highlights how dividend growth equities tend to outperform the market with reduced risk. Even high-yield stocks offer better performance than the market average.

Vanguard

The fundamental goal is to outperform the market during bear phases. Protecting against downturns when market conditions deteriorate is essential for achieving long-term investment success, even if stocks don’t consistently outperform during bull runs.

While predicting stock performance in bear markets remains uncertain, focusing on companies with robust business models, solid balance sheets, and a strong potential for dividend growth can significantly enhance the odds of successful investing, even amidst disappointing economic growth.

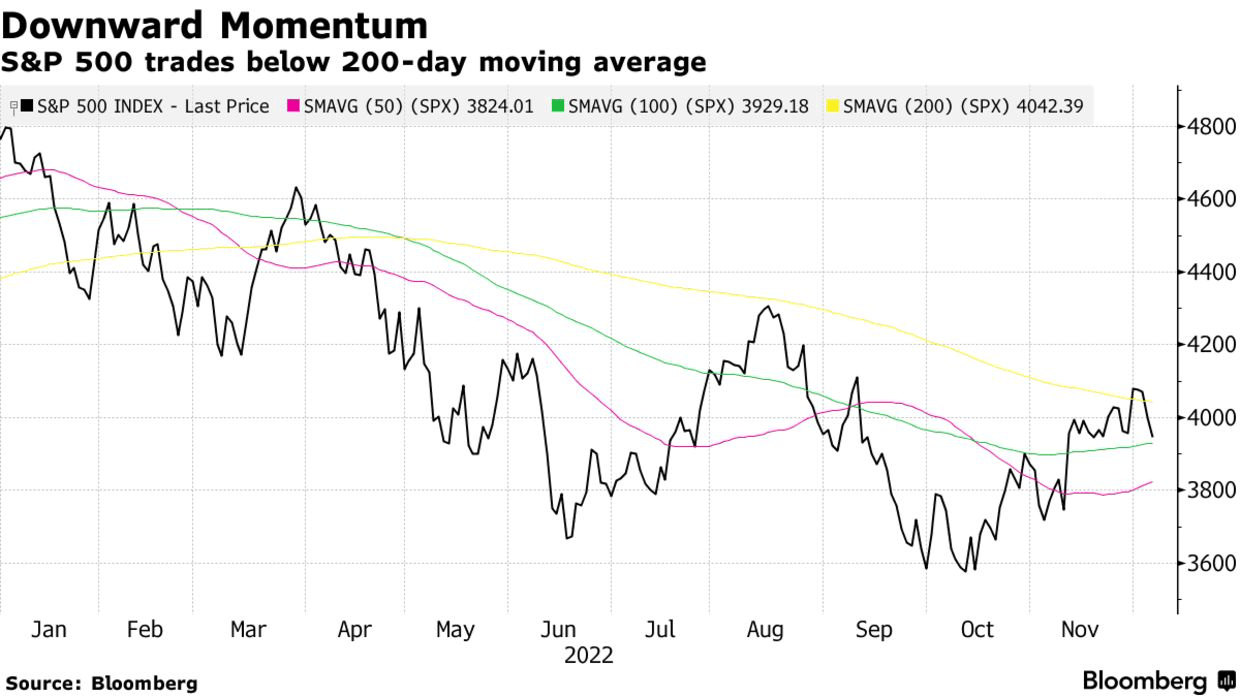

Before diving into the specific stocks I recommend, let’s briefly examine the current landscape. We find ourselves in a period of high uncertainty, characterized by elevated inflation, sharply declining economic growth, and the Federal Reserve’s continued commitment to raising interest rates in an attempt to combat inflation.

Cracks are emerging in the housing market, labor market, and other sectors that have supported the bull market since 2009.

Bloomberg

Recent insights from Bloomberg highlight a range of perspectives:

From David Solomon of Goldman Sachs Group Inc. cautioning about “bumpy times ahead,” to Jamie Dimon of JPMorgan Chase & Co. expressing a more pessimistic outlook predicting a “mild to hard recession,” and Lisa Shalett of Morgan Stanley Wealth Management suggesting corporations are in for a “rude awakening” regarding earnings, the overall sentiment has grown increasingly negative.

While I don’t adopt a bearish stance—especially for the long term—my position is that stock prices may need to decline further to adequately reflect economic risks and prompt the Federal Reserve to adjust its course.

Bloomberg

However, one significant risk remains: the unpredictable nature of the market.

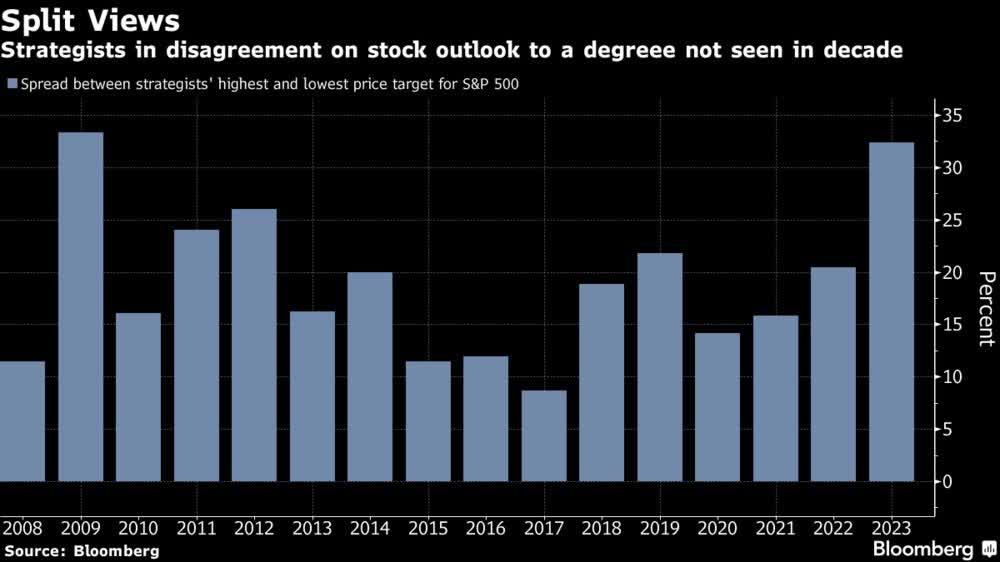

On one hand, experts suggest we might be nearing a market bottom as the Fed funds rate approaches its peak. On the other, there are those who argue we have yet to see the worst.

This divergence has led to the most significant gap in S&P 500 projections for 2023 since 2009.

Bloomberg

The outlook for 2023 is uncertain; it could be negative, but it might also yield typical results if the Fed pivots and possibly resumes quantitative easing, depending on how the economic situation unfolds.

In essence, my investment strategy remains unchanged. I invest in stocks on my watchlist whenever I find their valuations appealing. Should prices decline further, I plan to average down. The key adjustment I’ve made is increasing my savings rate and cash reserves. This enables me to capitalize on buying opportunities if market conditions deteriorate.

With this background, let’s explore the three stocks I recommend, known for their safety, dividend payouts, and strong potential for long-term outperformance.

These stocks are suitable for everyone, from casual investors to seasoned financial professionals, aiming to outperform the market while generating income.

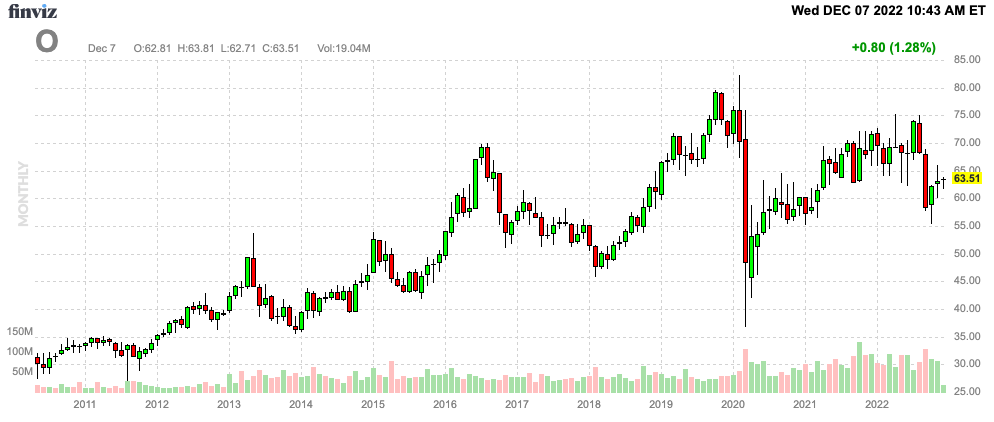

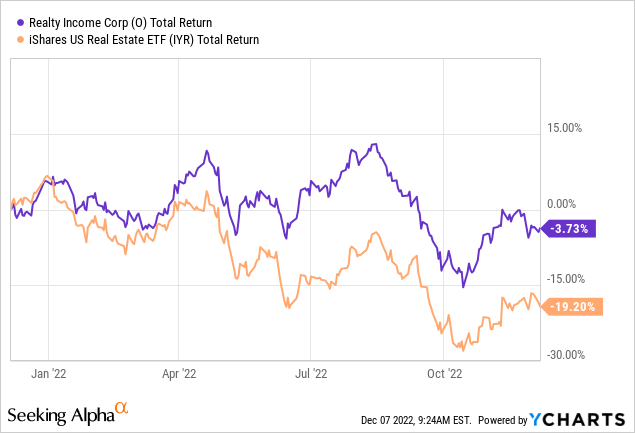

1. Realty Income (O) – Attractive 4.7% Yield

FINVIZ

While Realty Income has not previously been a part of my portfolio, my investment strategy has evolved to include higher-yield options for tax considerations. Fortunately, the market has presented some outstanding opportunities in this category, and Realty Income stands out among them.

Often referred to as the “monthly dividend company,” Realty Income ranks among the top five global REITs. This dividend aristocrat has delivered an impressive 14.6% compounded annual total return since 1994, with an average annual dividend increase of 4.4% over the same period.

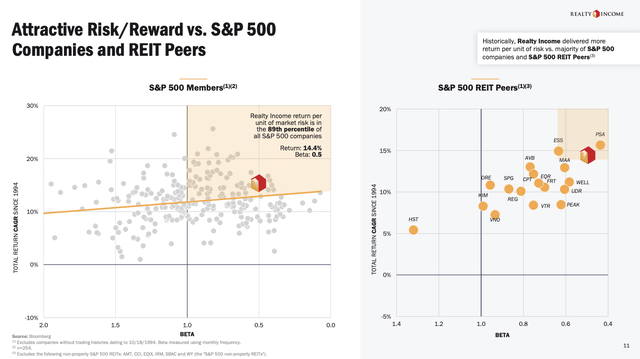

Realty Income boasts a compelling compounded annual return of 14.4% since 1994. With a beta of just 0.5, the company demonstrates exceptional performance on a volatility-adjusted basis, particularly when compared to its REIT peers, showcasing subdued volatility alongside strong long-term returns.

Realty Income

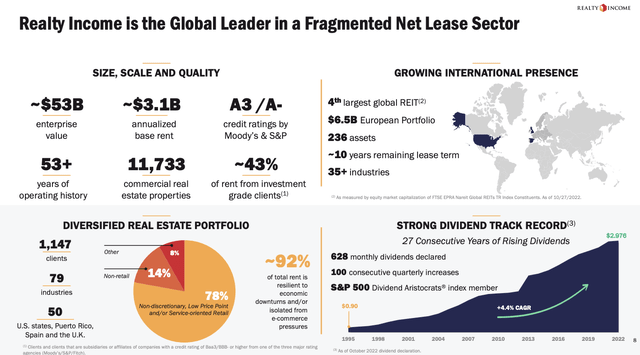

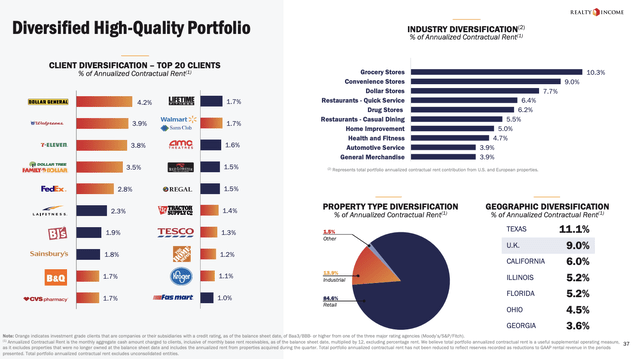

Moreover, Realty Income is among the few REITs with an A-rated balance sheet. Approximately 43% of its 1,147 clients are investment-grade, and the company owns assets across 79 diverse industries in all 50 states.

Realty Income

Despite the challenges posed by a high-interest rate environment, Realty Income is capitalizing on a robust sale and leaseback trend, where large companies are outsourcing their real estate needs. For instance, Realty Income recently acquired the Encore Boston Harbor Resort and Casino for $1.7 billion at a 5.9% cash cap rate from Wynn Resorts (WYNN), marking the company’s inaugural venture into casino properties.

This acquisition demonstrates Realty Income’s commitment to diversifying its portfolio beyond traditional retail assets by seizing opportunities in sale and leaseback transactions.

Additionally, my previous reservations regarding Realty Income stemmed from the significant pressure on smaller retail stores, a situation exacerbated by the pandemic. However, Realty Income’s top-tier tenants and strong presence in defensive sectors reliant on brick-and-mortar establishments are vital components of its resilience.

Realty Income

Moreover, another key factor contributing to the O ticker’s strong performance relative to its peers is the company’s exceptional balance sheet.

The company’s outstanding rating from both Moody’s and S&P Global underscores its financial strength. With a leverage ratio of just 5.2x, 95% of its debt is unsecured, and 88% is fixed-rate, with an average maturity of 6.3 years for its notes and bonds.

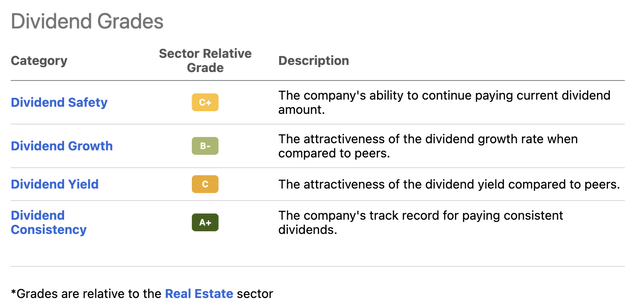

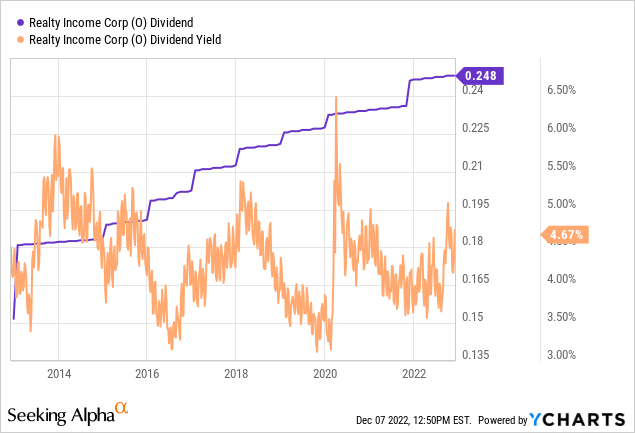

Realty Income’s Seeking Alpha dividend scorecard reflects a respectable yield of 4.7%, based on a monthly dividend of $0.248 per share.

Seeking Alpha

Over the past decade, the average annual dividend growth rate has reached 5.6%, which surpasses the long-term average of 4.4% since its initial public offering in 1994.

Now, let’s move on to the second stock on our list.

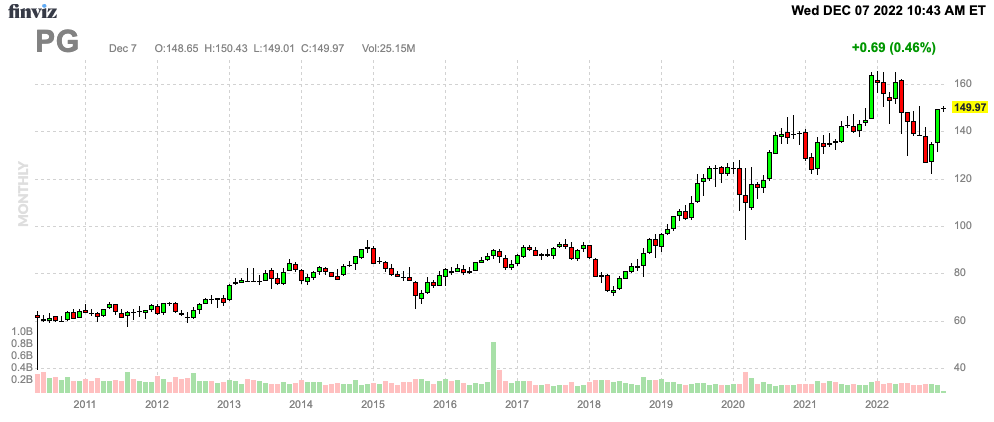

2. Procter & Gamble (PG) – Reliable 2.4% Yield

FINVIZ

When seeking a stock with a robust business model, consistent yield, sustainable dividend growth, a solid balance sheet, and the potential for long-term capital gains, Procter & Gamble emerges as a top contender.

Founded in 1837 and headquartered in Cincinnati, Ohio, Procter & Gamble has established itself as one of the oldest and most reputable consumer goods companies globally, boasting a market capitalization of $359 billion.

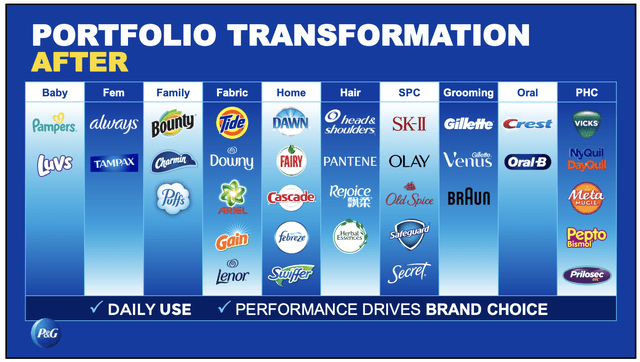

Procter & Gamble owns a portfolio of some of the world’s most recognized consumer brands across various categories, including Baby products like Pampers, household essentials like Tide fabric softener, and oral care products like Oral-B.

Procter & Gamble

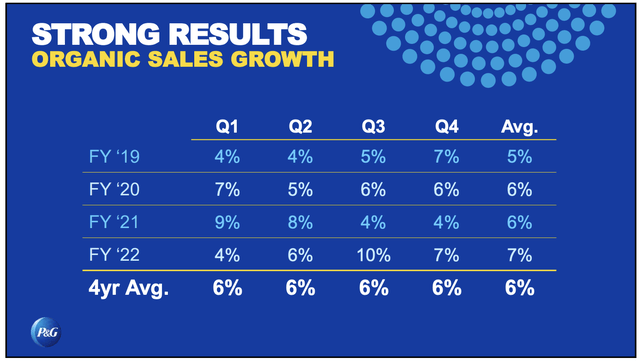

These popular products have enabled the company to achieve an organic volume growth rate of 3% annually over the past four years. When factoring in pricing, organic sales growth has averaged 6% per year, leading to an impressive 9% annual core EPS growth during this timeframe.

Procter & Gamble

The company has not recorded a single quarter of negative organic sales growth since tracking commenced in the dataset.

Even amidst the current climate of high inflation and declining consumer health, Procter & Gamble remains resilient. For the 2023 fiscal year, the company anticipates core EPS growth between 0% and 4%, with organic sales growth projected to be no less than 3%. After adjusting for currency fluctuations, core EPS is expected to rise by at least 9%.

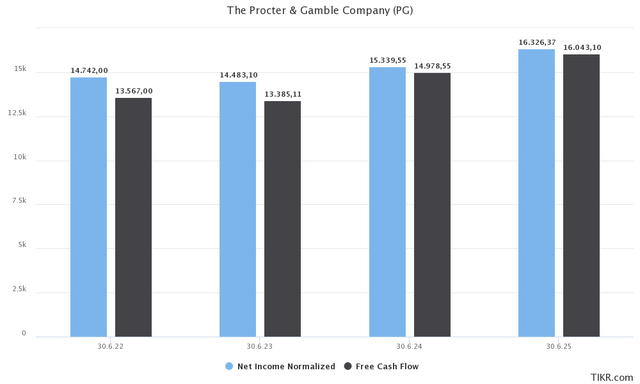

Procter & Gamble’s strong cash generation capabilities are noteworthy, consistently maintaining free cash flow close to 100% of net income. In the 2024 fiscal year, the company expects to generate approximately $15 billion in free cash flow, translating to a 4.2% free cash flow yield based on its $359 billion market capitalization.

TIKR.com

Procter & Gamble has maintained its dividend distribution for an impressive 132 years, boasting 66 consecutive years of dividend increases. Over the last decade, the company has returned a staggering $141 billion through dividends and stock repurchases.

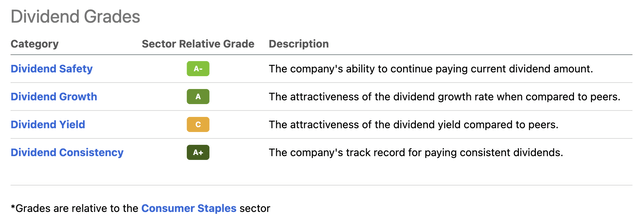

Despite its relatively low yield compared to the consumer staples sector, Procter & Gamble’s Seeking Alpha dividend scorecard remains highly appealing. The yield is somewhat underwhelming when compared to other slow-growing, high-yield stocks in the sector. However, I prioritize growth over yield in most instances.

Seeking Alpha

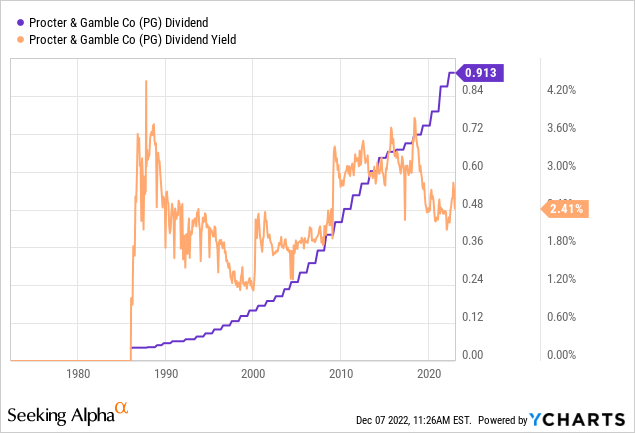

Procter & Gamble offers a quarterly dividend of $0.9133 per share, translating to a yield of 2.4%. This yield is below pre-pandemic levels.

Over the past decade, the average annual dividend growth rate stands at 5.0%, with the rate increasing to 6.9% over the past three years.

The most recent dividend increase was announced in April of this year, with management implementing a 5.0% hike.

The cash flow payout ratio is currently 50%. Net debt is projected to reach $25.8 billion by the end of the current fiscal year, which equates to just 1.2 times EBITDA.

Thanks to its robust business model, high free cash flow, and manageable debt levels, Procter & Gamble holds an Aa3 credit rating, surpassing the ratings of some developed nations.

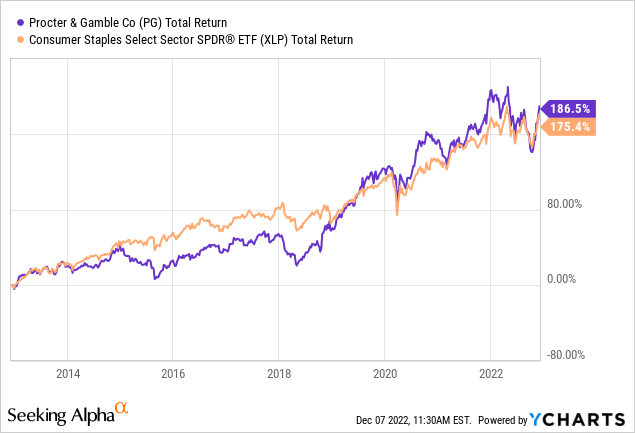

Additionally, the company has outperformed the Consumer Staples ETF (XLP) by over 10 percentage points in the past decade.

Before we delve into the performance of P&G in terms of volatility-adjusted returns, let’s examine the third stock on our list, which I have held since 2020.

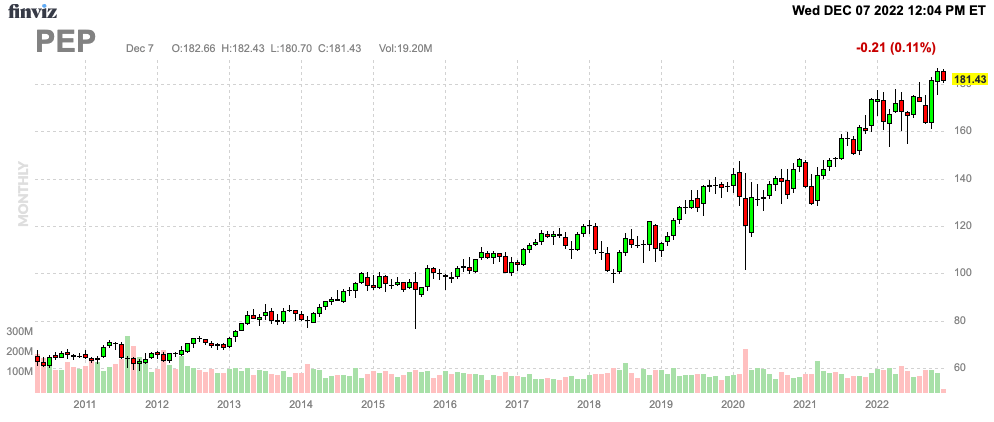

3. PepsiCo (PEP) – Consistent 2.5% Yield

FINVIZ

PepsiCo is one of the initial five stocks I acquired when I began my dividend growth portfolio in 2020. With a market capitalization of $253 billion, it stands as another major player in the consumer staples sector. Unlike Procter & Gamble, its product lineup includes both beverages and snacks.

In September, I authored an article titled “2 All-Weather Dividend Stocks You Should Own,” featuring PepsiCo for its robust pricing power and capacity to deliver consistent value. Despite facing challenges such as high inflation, poor consumer health, and a proactive Federal Reserve, PEP shares have risen nearly 5% year-to-date.

PepsiCo boasts an A+ credit rating and a business model characterized by strong pricing power.

The company, which includes well-known brands like Lay’s, Tropicana, Pepsi, and Quaker, reported an impressive 16.0% organic revenue growth in the third quarter, with its Frito-Lay North America division achieving a remarkable 20% organic sales growth. Notably,

Sienna Blake is a licensed aesthetic consultant and beauty writer specializing in cosmetic surgery advancements and non-invasive treatments. With a background in dermatology and over eight years of industry experience, Sienna is passionate about helping people achieve confidence through informed beauty decisions. She holds a Bachelor's degree in Health Sciences and regularly collaborates with top plastic surgeons to stay at the forefront of aesthetic innovations. Outside of her work, Sienna enjoys traveling, skincare research, and practicing Pilates.