97/E+ via Getty Images

Comprehensive Investment Analysis of Henkel

Henkel (OTCPK:HENKY) is currently navigating a challenging landscape following a series of operational headwinds. In 2019, the company struggled to achieve organic growth, and profit margins experienced a slight decline. The challenges escalated with the onset of the coronavirus pandemic, which saw a notable decrease in sales, particularly in the Adhesive Technologies segment, where a sales drop of 8.21% was recorded. Additionally, profit margins suffered considerably due to lower volumes coupled with increased growth investments, especially in marketing efforts. Although sales showed recovery in 2021, persistent issues such as supply chain disruptions, inflationary pressures, and labor shortages continued to suppress margins. As of 2022, the ongoing Russia-Ukraine conflict has introduced additional operational risks, particularly as the company ceased its operations in Russia amidst intensifying inflationary challenges.

Nevertheless, Henkel has remained proactive, pursuing acquisitions and effectively reducing its debt over recent years. The decline in share prices, attributed to short-term headwinds, has coincidentally led to an increase in the dividend yield. It is crucial to recognize that Henkel has been a reputable business since 1876, with products that have integrated into the lives of consumers over generations. This article will delve into the reasons why the current challenges, linked closely to the broader macroeconomic environment, present a favorable opportunity for long-term dividend growth investors.

Understanding Henkel’s Global Operations and Market Position

Henkel stands as a premier global manufacturer, specializing in a diverse range of products, including adhesives, beauty care, and laundry and home care solutions, with operations spanning across the globe. Established in 1876, the company boasts a current market capitalization of approximately €28 billion and employs over 50,000 individuals worldwide. Its business operations are organized into three primary segments: Adhesive Technologies, Beauty Care, and Laundry & Home Care, each contributing uniquely to the company’s overall performance.

Henkel logo (Henkel.com)

Within the Adhesive Technologies segment, which accounted for 48% of the company’s sales in 2021, Henkel produces a variety of adhesives, sealants, and functional coatings. These products cater to diverse industries such as packaging, consumer goods, automotive, electronics, and construction. Key brands in this segment include Loctite, Technomelt, Bonderite, Teroson, and Aquence. The Beauty Care segment, contributing 18% to sales, focuses on hair cosmetics and personal care products, marketed primarily through retail channels and direct-to-consumer platforms under notable brands like Schwarzkopf, Dial, and Syoss. The Laundry & Home Care segment, which made up 33% of sales, encompasses a wide range of household products, including detergents, fabric softeners, and cleaning agents, with well-known brands such as Persil, Bref, and Purex.

Henkel remains committed to innovation, continuously launching new products to align with evolving market demands. Recently, the company introduced a silicone-free liquid thermal gap filler designed to enhance the lifespan of automotive batteries, particularly targeting the burgeoning electric vehicle market. This initiative exemplifies Henkel’s dedication to investing in technology startups and advancing its product offerings to meet contemporary consumer needs.

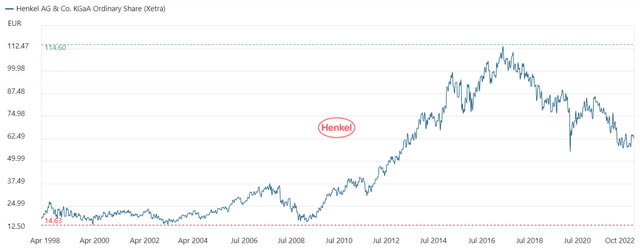

Henkel ordinary share prices (Henkel.com/investors-and-analysts/shares/share-prices)

Currently, Henkel’s ordinary shares are trading at €63.00, reflecting a significant decline of 45.03% from the peak of €114.60 reached in June 2017. This decrease has led to a considerable rise in the dividend yield, now at 2.94%, suggesting ample potential for growth given that the company allocates a modest portion of its cash flow to dividends. This article will explore the case for Henkel as a resilient dividend stock suitable for long-term holding, while also reviewing the company’s recent expansion initiatives.

Strategic Acquisitions and Divestitures Fueling Growth

Henkel’s growth strategy has heavily relied on strategic acquisitions, including the purchase of The Sun Products Corporation for approximately €3.2 billion in 2016 and the acquisition of Zotos International, Shiseido’s North American Hair Professional division, for $485 million in 2017. These initiatives have enabled the company to significantly lower its debt levels during the 2018-2021 period while also pursuing smaller acquisitions to enhance its market presence.

In more recent developments, Henkel agreed to acquire a 75% stake in Invincible Brands Holding in July 2020, which comprises three rapidly growing premium direct-to-consumer brands: HelloBody, Banana Beauty, and Mermaid+Me, primarily marketed in Europe. In November 2020, the company expanded its portfolio by acquiring skin model technology from SkinInVitro GmbH, enhancing its capabilities in the realm of reconstructed human tissue models.

In June 2021, Henkel divested its non-core brands Right Guard and Dry Idea from its Beauty Care segment, subsequently acquiring Swania SAS, a fast-growing French manufacturer of sustainable laundry and home care products, which generated approximately €40 million in sales in 2020. The company further strengthened its position in the Asia-Pacific region by acquiring Shiseido’s Hair Professional business in February 2022, which reported around €100 million in sales in 2020, boasting a strong foothold in Japan, China, and South Korea.

In September 2022, Henkel made significant strides by acquiring NBD Nanotechnologies Inc., a cutting-edge US-based startup specializing in advanced materials with applications across various sectors including electronics, consumer goods, and automotive. Additionally, the company acquired the Thermal Management Materials business of Nanoramic Laboratories, focused on innovative energy storage and thermal management solutions. These acquisitions reflect Henkel’s commitment to investing in high-growth sectors and enhancing its product portfolio.

Sales Growth Trends Over the Past Decade

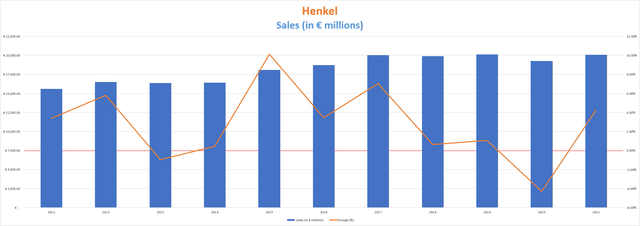

Over the past decade, Henkel has experienced a gradual, yet consistent sales increase, largely attributed to its strategic acquisitions. However, sales stagnated between 2017 and 2021, a period predominantly characterized by a focus on debt reduction. This strategic move is now poised to usher in a new chapter of growth, enabling Henkel to explore additional acquisitions that will drive future sales growth.

Henkel sales (Annual reports)

Despite a recent plateau in sales, 2022 has emerged as a promising year for Henkel, with sales surging by 9.9% year-over-year in the first half, and a remarkable 17.36% increase in the third quarter, reaching €5,976 million—marking the highest quarterly sales in Henkel’s history. This growth was fueled by a robust 16.8% organic sales boost in the Adhesive Technologies segment. Importantly, the company raised prices across all business segments, successfully offsetting the decline in Russian sales, which accounted for ~5% of total sales prior to the conflict. However, there was a slight dip in sales volume of -3.4% year-over-year during the third quarter.

Henkel’s expansion strategy extends beyond acquisitions; the company is actively constructing new manufacturing facilities to enhance production capabilities globally, alongside establishing R&D centers to drive innovation. Furthermore, Henkel’s sales stability is underpinned by strong brand loyalty, as customers recognize the high quality and value of its products. In 2021, sales distribution revealed that 41% originated from emerging markets, with 30% from Western Europe, 25% from North America, and 3% from Japan, Australia, and New Zealand. This diverse geographical footprint decreases exposure to competition from private labels, particularly in emerging markets where such consumption is less prevalent.

Understanding Margin Trends and Profitability

Over the past decade, Henkel has maintained an EBIT margin above 10%, surpassing the 15% threshold in 2017 and 2018. However, challenges stemming from the coronavirus pandemic, along with ongoing supply chain disruptions, inflationary pressures, and labor shortages, have led to a noticeable decline in both gross and EBIT margins in 2020 and 2021, although gross margins remain close to 45%. This underscores the company’s strong profitability even amidst adversities.

Henkel gross and EBIT margins (Annual reports)

In 2021, gross margins dipped to 44.7%, with EBIT margins at 11.0%. For 2022, management anticipates EBIT margins to fluctuate between 10% and 11%, indicating a slight decline compared to 2021, despite strong pricing strategies. It is crucial to note that approximately 30% of sales are generated from operations in Europe, where inflationary pressures due to the Russia-Ukraine conflict significantly impact the company’s operations. Increasing energy costs in Europe present a substantial challenge, with no immediate resolution in sight. The management team is currently exploring further pricing adjustments to mitigate these increased costs, ensuring continued debt repayment.

Demonstrating Profitability Through Effective Debt Management

Henkel’s impressive profitability is illustrated by its capacity to effectively manage and reduce debt post-major acquisitions. The company has successfully decreased total borrowings by 35%, bringing the figure down to €2.84 billion between 2017 and 2021, positioning itself for a new growth phase through further acquisitions, such as the recent purchase of Shiseido’s Hair Professional business in Asia-Pacific. The reduction of debt to €2.84 billion in 2021 suggests that Henkel is strategically poised for increased sales through new acquisitions, although the pace of debt reduction has slowed due to an uptick in the dividend payout ratio stemming from lower cash flow resulting from diminished profit margins.

Management has proactively implemented pricing strategies in recent quarters to reflect the inflationary environment affecting the company’s products. However, these measures have not completely offset the decline in profit margins due to persistent inflationary pressures. Future price increases are anticipated to help stabilize margins; however, increased production costs persist as long as inflation remains a concern in the market.

Ensuring Dividend Stability Amidst Economic Challenges

Henkel’s dividend policy stipulates an annual payout ratio ranging from 30% to 40% of net income after accounting for non-controlling interests. This policy reflects a commitment to returning value to shareholders while balancing financial health.

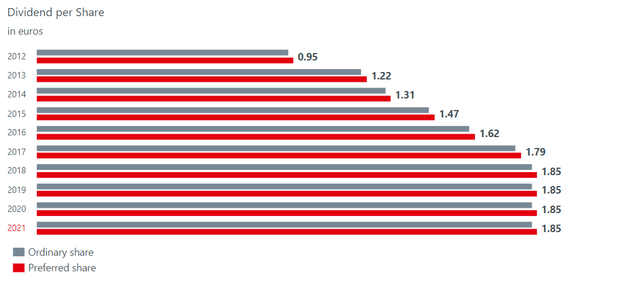

Henkel dividends per share (Henkel.com/investors-and-analysts/shares/dividends)

The company has consistently increased its dividend payout from €0.95 in 2012 to €1.85 in 2019, marking a remarkable 95% rise over seven years. However, the dividend was frozen for 2020, 2021, and 2022 due to mixed results in 2019, the impact of the coronavirus pandemic, subsequent supply chain challenges, and the ongoing conflict between Russia and Ukraine, which has exacerbated the headwinds faced in 2021.

The intensifying challenges have placed the current annual dividend of €1.85 under scrutiny, as cash from operations fell to €177 million in the first half of 2022, down from €685 million in the same period of 2021. This decline explains the sluggish recovery of shares following the initial shock of the pandemic and the inflationary pressures encountered in 2021. Nevertheless, inventories rose by €426 million year-to-date, accounts receivable increased by €492 million, while accounts payable grew by only €389 million.

To assess the sustainability of the dividend, I have calculated the cash payout ratio over the years, indicating the percentage of cash from operations allocated to dividend payments. This analysis provides insights into the company’s ability to maintain dividend payments through operational performance.

| Year | 2013 | 2014 | 2015 | 2016 | 2017 | 2018 | 2019 | 2020 | 2021 |

| Cash from operations (in millions) | €2,116 | €1,914 | €2,384 | €2,850 | €2,468 | €2,698 | €3,241 | €3,080 | €2,141 |

| Dividends paid (in millions) | €407 | €525 | €564 | €633 | €698 | €772 | €798 | €798 | €798 |

| Cash payout ratio | 19.23% | 27.43% | 23.66% | 22.21% | 28.28% | 28.61% | 24.62% | 25.91% | 37.27% |

The data reveals that Henkel has consistently maintained a low cash payout ratio over the years, allowing the company to pursue acquisitions and effectively reduce debt levels. Despite the significant decline in EBIT margin in 2021, the cash payout ratio stands at a healthy 37%. From a cash flow perspective, the dividend appears secure; however, shareholders may need to temper expectations for substantial dividend growth in the near term until the current geopolitical and inflationary challenges stabilize. Adjusted net income fell by 19.3% year-over-year to €840 million in the first half of 2022, emphasizing the need for cautious optimism. Thus, Henkel presents an attractive investment opportunity for dividend investors with a long-term perspective, especially given the current share price decline, which has resulted in a dividend yield of 2.94% in a historically solid company.

Identifying Key Risks in Henkel’s Business Model

The risks faced by Henkel have escalated notably over the past few years, particularly throughout 2020, 2021, and 2022. Shareholders must recognize these risks, which may offset the perceived value of the current discounted share prices.

- While Henkel successfully reduced its debt during 2018-2021, the existing debt level remains significant enough to restrict the pace of future acquisitions in the short to medium term, despite cash from operations comfortably covering dividend payouts.

- The company’s recovery is closely tied to the resolution of the Russia-Ukraine conflict. Even after the conflict ends, lingering effects such as inflationary pressures, increased energy costs, and revenue losses from exiting the Russian market could persist for an extended period.

- Given the management’s conservative approach regarding the payout ratio, dividends may remain frozen for several years. Investors should not anticipate further increases until the company significantly reduces its debt and stabilizes profit margins. The adjusted net income fell by 19.3% year-over-year in the first half of 2022, which is crucial for determining the company’s dividend growth potential.

Evaluating Investment Potential for Long-Term Dividend Growth

In my assessment, the current share prices present an attractive opportunity for dividend growth investors to consider acquiring Henkel shares. A dividend yield on cost of approximately 3% for a company with a historically low cash payout ratio below 30% is a generous offering, especially in light of the ongoing challenges faced in 2021 and 2022, where the cash payout ratio has approached 40%.

These challenges are largely temporary, attributable to the impacts of the coronavirus pandemic in 2020, subsequent supply chain disruptions and inflationary pressures in 2021, and the current geopolitical tensions related to the Russia-Ukraine conflict. Henkel’s legacy as a company operating for nearly 150 years, combined with its strong brand portfolio, suggests resilience. Moreover, the consistent reduction in debt since 2018, bolstered by strong profitability, positions Henkel for further acquisitions that could enhance future sales growth. Therefore, the 45.03% decline in share price represents a strategic opportunity for investors seeking to enrich their dividend growth portfolios with a long-term focus.